When you accrue interest as a lender or borrower, you create a journal entry to reflect the interest amount that accrued during an accounting period. This journal entry is made to eliminate the interest payable that we have recorded previously from the balance sheet. Here’s the journal entry the company passes for interest expense and interest payable on the balance sheet. At the end of the second month, the company would pass the same entry, and as a result, the interest payable account balance would be $40,000. The time of paying interest will depend on the loan schedule agreed between borrower and lender.

Journal entries:

The interest expense record on the income statement is prepared at the end of the month. Accurately calculating the interest payable is essential for businesses to ensure that they are properly tracking their financial obligations. It is also important to consider other related factors such as the payment date and any applicable fees when calculating the total interest payable. Company ABC borrowed $200,000 from creditors and must pay $5,000 interest per month in accordance with the contract. Furthermore, keeping accurate records of interest payable can help the company to better manage its cash flow and to make sure that all payments are made on time. Reversing a journal entry is most common for entries for for recurring expenses or revenues.

What Is AccountsBalance?

- For these types of debts, the interest rate is usually fixed at an average of 8-13%.

- Failure to accurately report interest payable can lead to penalties imposed by the IRS.

- The accumulated interests are quite commonly recorded when one deals with a bond instrument.

- An advertising agency signs a $6,000, 3-month note payable (a type of loan) with an annual rate of 10% on October 1st.

- Debiting an accrued expense and crediting a liability account accurately reflects the financial obligation a company has incurred for interest payments.

The accumulated interests are quite commonly recorded when one deals with a bond instrument. As the company has not yet made a payment, it will create interest payable on balance sheet. At the end of the accounting period, company calculates the interest expense base on the principle and interest rate. After that company will record interest expense into income statement while the other side impacts the interest payable.

Ultimate Accounting Cheat Sheet for Small Business Owners

The most crucial part is that it is entirely different from interest expense. When a company borrows an amount from a financial institution, it must pay an interest expense. However, a company can’t show the entire amount of interest expense on the balance sheet. It can only show the interest amount that’s unpaid until the reporting date of the balance sheet. Interest payable can include both billed and accrued interest, though (if material) accrued interest may appear in a separate “accrued interest liability” account on the balance sheet. Interest is considered to be payable irrespective of the status of the underlying debt as short-term debt or long-term debt.

Deskera payroll automation is an intuitive, user-friendly software you can use to automate not just expenses, but almost every part of your accounting process. A construction company takes out a 12-month bank loan of $60,000, with a rate of 8%. Interest payable is the amount of interest on its debt that a company owes to its lenders as of the balance sheet date.

Interest payable can incorporate costs that have already been charged or the costs that are accrued. The general ledger account for Notes Payable has been reduced by the amount of the principal portion of the payment, and should agree with the amortization schedule. Company ABC borrows $ 100,000 from the bank with an interest rate of 6% per year. The company has to pay the interest expense of $ 500 per month, it is paid on the 5th of each month. The interest payments on a loan can have a significant impact on the income statement if the company relies on debt rather than equity.

They would also need to tell us the amount of interest expense, which would be under U.S. The payable account would be zero after the interest expenditures are paid, and the corporation would credit the cash account with the amount paid as interest expense. It represents interest stimulus payments payable on any borrowings—bonds, loans, convertible debt or lines of credit. Notes Payable is a liability account that reports the amount of principal owed as of the balance sheet date. This journal entry is used to accurately track the company’s financial obligations.

Interest expenses are debits because in double-entry bookkeeping debits increase expenses. Credits, in this case, are usually made for interest payable since that account is a liability, and credits increase liabilities. With the accrual basis of accounting, you record expenses as they occur, not when you pay.

Entries to the general ledger for accrued interest, not received interest, usually take the form of adjusting entries offset by a receivable or payable account. Interest payable is a liability that represents the amount of interest owed to creditors but not yet paid. It can be classified as either short-term or long-term, depending on when the interest is due. Short-term interest payable is due within one year, while long-term interest payable is due more than one year from the balance sheet date. Interest payable is typically combined with other current liabilities on the balance sheet, but it may also be presented as a separate line item. In addition, it is important to note that the interest payable journal entry must also be recorded in the general ledger.

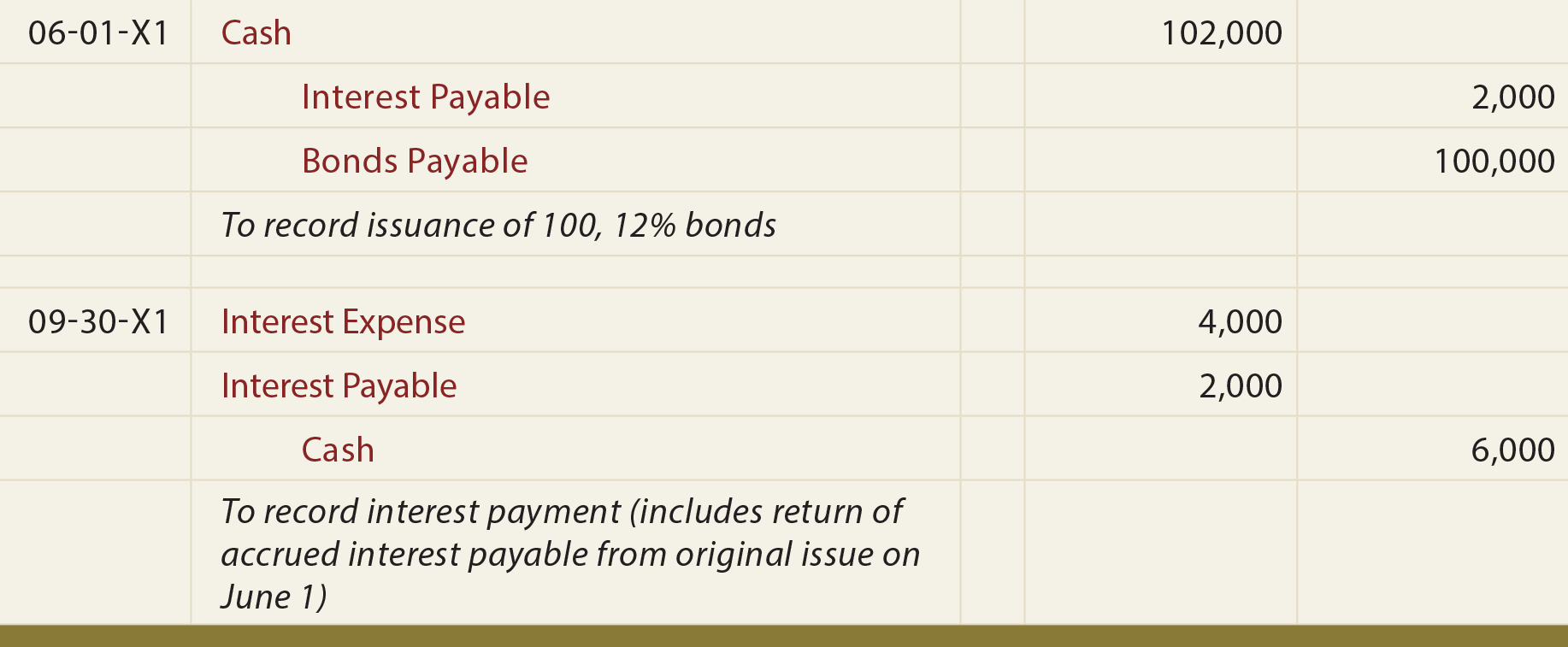

The company’s journal entry credits bonds payable for the par value, credits interest payable for the accrued interest, and offsets those by debiting cash for the sum of par, plus accrued interest. The use of accrued interest is based on the accrual method of accounting, which counts economic activity when it occurs, regardless of the receipt of payment. This method follows the matching principle of accounting, which states that revenues and expenses are recorded when they happen, instead of when payment is received or made. Maria will repay the principal amount of debt plus interest @ 15% on April 30, 2021, on which the note payable will come due.

Interest coverage ratio is calculated by dividing (earnings before interest and taxes) by (total outstanding interest expenses). Interest payable and interest expense are terms that are most often confused in their usage. Though they are meant for serving almost same objectives, there are differences that must be known to firms and individuals using them. Welcome to AccountingFounder.com, your go-to source for accounting and financial tips. Our mission is to provide entrepreneurs and small business owners with the knowledge and resources they need. As you can see the interest payable is decreasing and cash on hand or cash in the bank is decreasing as well in the same amount.